近日,招商银行私人银行部总经理王晏蓉出席了中国财富管理50人论坛2023年会(第十届)并在“养老金融:多层次养老保障体系应对长寿时代”主题论坛上发表题为《新形势下养老金融的实践与探索》的演讲。

王晏蓉表示,我国加速迈入老龄化时代。与国际水平相比,我国养老金的储备总量非常不足。养老产品与政策目前仍存在一些问题。做好养老金融这篇“大文章”需要全行业共同努力。需要出台更多的支持政策,包括对低收入人群进行财政补助和贴息、养老产品享受税收减免,以及提高个人养老金免税缴存上限。国家层面上,要加大宣传力度,包括提高居民的风险防范意识和强化居民的养老意识。监管引导方面,需要加强监管引导,鼓励机构大力投入养老。此外,银行业、保险业、基金业和信托业等金融机构在养老金融领域发挥各自优势。

党的二十大报告提出“发展多层次、多支柱的养老保险体系”,实施积极应对人口老龄化的国家战略,发展养老事业和养老产业,优化孤寡老人的服务,推动实现全体老年人享有基本的养老服务。

2022年11月,国家出台《个人养老金实施办法》。2023年10月底召开的中央金融工作会议明确将“养老金融”纳入金融发展的“五篇大文章”,为金融机构做好养老金融相关工作指明了方向,提供了根本遵循和行动指南。

一、我国加速迈入老龄化时代

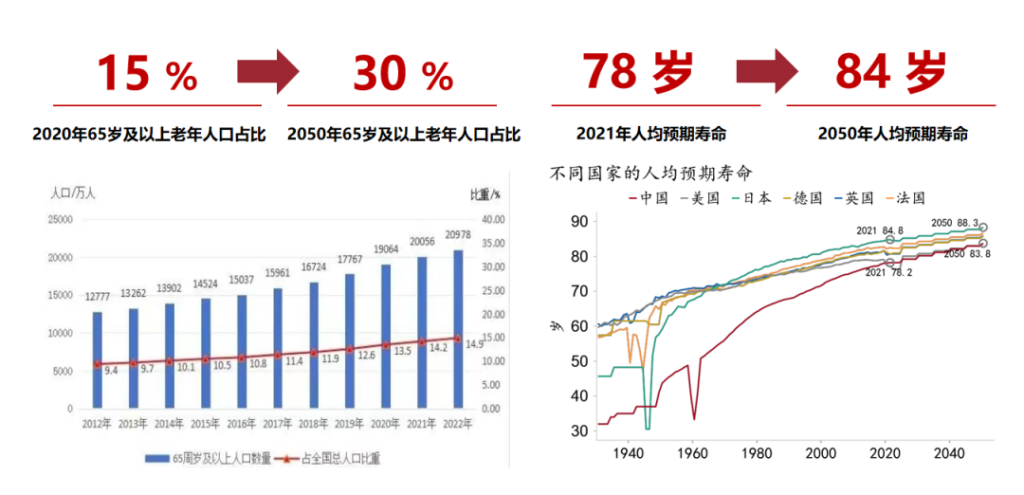

2020年,65岁以上的老年人口占比15%,按照目前的人口发展趋势,预计到2050年,65岁以上的老年人口将占比30%,同时随着医疗技术的发展,2021年,人均寿命达到78岁,预计到2050年人均寿命将达到84岁。

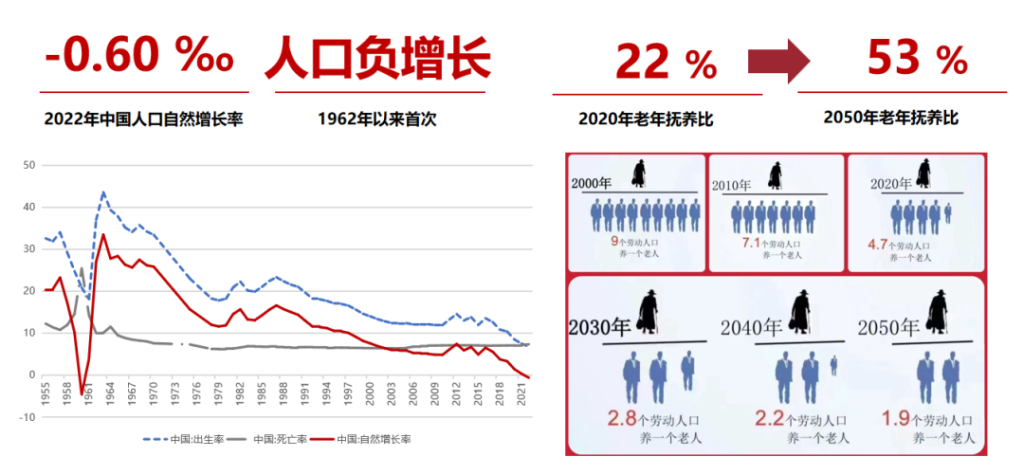

随着少子化、低生育率的持续,社会养老压力将进一步加剧。2022年,人口的自然增长率是负的千分之六,这是自1962年大灾荒时代后,第二次人口负增长。2020年,老年抚养比基本上是五个年轻人抚养一个老年人,预计到2050年,将由两个年轻人抚养一个老年人。现在缴纳养老金的人少,未来支出养老金的人多,这样的发展趋势是非常惊人的。

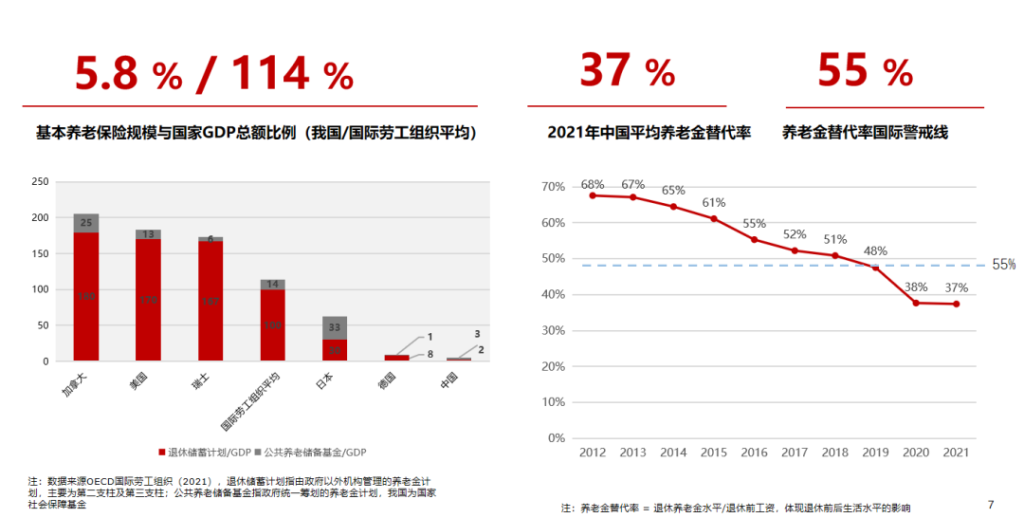

与国际水平相比,我国养老金的储备总量非常不足,我们目前的比例和国家GDP总额比只有3%,而国际劳工组织的平均水平14%,我们尚不足1/4。同时,养老金替代率的国际警戒线是55%,而我国在2021年就已经下降到了37%。可见目前的养老金替代率也是非常让人担忧的。 CXO UNION-CXO联盟(cxounion.cn)

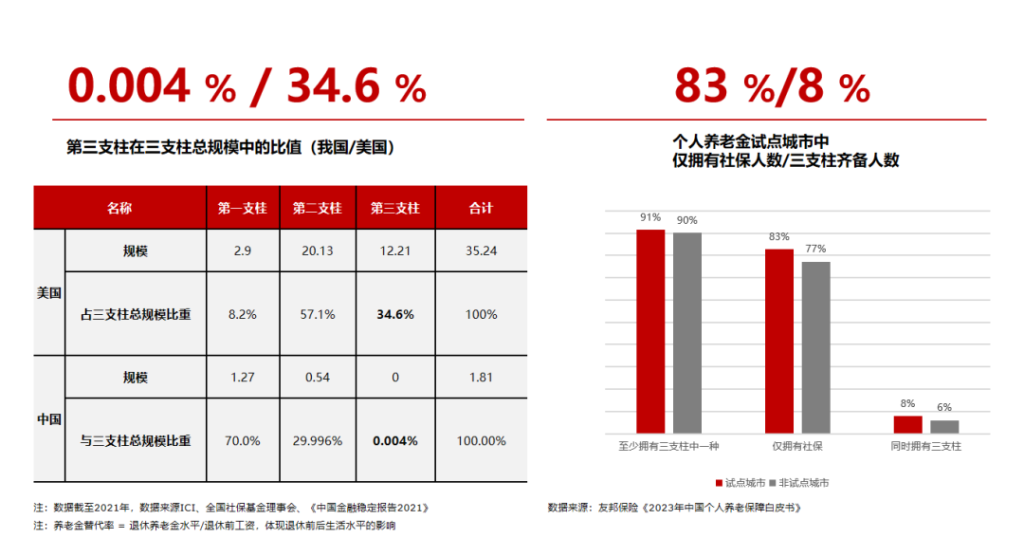

2022年,养老金第三支柱制度开始实施,这是一个良好的开始,但对比美国,美国的第三支柱占比34.6%,将近1/3,而我们只有十万分之四,是非常不足的水平。另外,我们有一个个人养老金的试点,目前三个支柱齐备的人口数量只有8%,仅有基础养老金的是83%,可见大家对“需要个人来积攒养老金”是缺乏重视的。

二、招商银行的养老金融实践

招商银行把养老金融作为招商银行的八大特色金融之一,另外结合个人养老的三个阶段,招商银行提供不同的工具和服务。在备老阶段,相对较年轻的人为自己的老年生活提前做准备,有个人养老金业务、养老产品的上架。如果客户已经到了退休年龄,属于享老阶段,需要我们与各类机构联合为客户提供养老社区和养老生活等方面的服务。针对老年人的一些财富传承,有家族信托和养老信托工具和产品。

从第三支柱个人养老金开户看,现在全市场一共有5094万人开通账户,目前招商银行的开户数是473.8万。从缴存金额看,全市场缴存了268亿元,户均缴存2000元,通过招行缴存的金额是63.7亿元,户均缴存7268元。

再看一下客户对于养老产品的选择情况。 CXO UNION-CXO联盟(cxounion.cn)

养老理财总量只有1004亿,占全市场的比例仅有千分之四左右,这说明养老产品在各类资管机构的产品中占比极低,也非常不足。虽然这是一个非常大的市场,但是未来我们需要共同努力;养老理财占全市场理财产品的比例,也只有千分之三左右。保险,纯商业养老保险更少,占全市场比例只有万分之三左右。

我们得出的结论有以下四点:

第一,开户多,缴存少,凸显养老意识有待提升。从2022年10月至今,个人养老金呈现出“开户-缴费-投资”的倒金字塔结构,开户人超过4千万,缴存只有1千多万人,户均缴存金额仅有2000多元。可见大家在这方面的投资意识比较弱。

第二,个人养老金账户上限偏低。日本个人养老金账户(免税)上限为81.6万日元(约16万人民币);美国401k年度缴费上限6.6万美元(约47万人民币);而我国个人养老金(免税)上限仅为1.2万元人民币。

第三,养老金品种较少,大致是千分之三或者万分之三的水平。

第四,养老产品特色不突出。以养老基金为例,目前有179只养老基金,仅有10只实现了正收益,在表现负收益的产品中,亏损最大的基金收益为-18.38%。这让个人投资者产生担忧,进而对养老类产品产生排斥。

三、共同做好养老金融“大文章”

养老金融这篇“大文章”是需要我们全行业共同努力的。具体来看:

政策支持方面,需要出台更多的支持政策,包括对低收入人群进行财政补助和贴息、养老产品享受税收减免,以及提高个人养老金免税缴存上限。国家层面上,一定要加大宣传力度,包括提高居民的风险防范意识和强化居民的养老意识。监管引导方面,从监管层面一定要进行一些有效的引导,鼓励各个金融机构大力投入养老金融领域。

对于各个领域、各个行业来说,银行业,我们觉得重点是在特定养老目标理财发力,可以用住房反向抵押贷款等方式帮助大家注入一些养老资金的来源。 CXO UNION-CXO联盟(cxounion.cn)

保险业方面,除了以泰康为主的社区养老,现在有很多保险公司在这个领域发力。我们觉得未来还有很多比较大的文章去做,包括居家养老、失能失智老人的养老和护理类的养老等。

基金业,除了要做大做强养老目标基金的方向,在养老产业引导基金、股权基金等方面空间也比较大。

从信托业来说,重点在特殊目的信托,如养老信托,这一块的市场潜力也非常大。

最后一句话,金融也应该携手前行,砥砺奋进,全行业共同努力,写好养老金融“大文章”,共同迎接养老金融的美好时代。

翻译:

Wang Yanrong, China Merchants Bank: How do financial institutions play their advantages in the field of pension finance?

Recently, Wang Yanrong, general manager of the Private Banking Department of China Merchants Bank, attended the China Wealth Management 50 Forum 2023 Annual Meeting (10th session) and delivered a speech entitled “Practice and Exploration of Pension Finance under the New Situation” at the theme forum of “Pension Finance: Multi-level Pension Security System to cope with the Age of Longevity”.

Wang Yanrong said that China is accelerating into the age of aging. Compared with the international level, the total amount of pension reserves in China is very insufficient. At present, there are still some problems in pension products and policies. To do a good job in pension finance this “big article” needs the joint efforts of the whole industry. More support policies are needed, including financial assistance and interest discounts for low-income people, tax breaks for pension products, and an increase in the tax-free contribution limit for personal pensions. At the national level, it is necessary to increase publicity efforts, including improving residents’ awareness of risk prevention and strengthening residents’ awareness of old-age care. In terms of supervision and guidance, it is necessary to strengthen supervision and guidance and encourage institutions to vigorously invest in elderly care. In addition, financial institutions such as the banking, insurance, fund and trust industries play their respective advantages in the field of pension finance. CXO UNION-CXO联盟(cxounion.cn)

The report of the 20th National Congress of the Communist Party of China proposed to “develop a multi-level and multi-pillar pension insurance system”, implement the national strategy of actively responding to the aging population, develop the pension service and the pension industry, optimize the service for the elderly, and promote the realization of basic pension services for all the elderly.

In November 2022, the state issued the Measures for the Implementation of Personal Pension. The Central Financial Work Conference held at the end of October 2023 clearly included “pension finance” into the “five major articles” of financial development, which pointed out the direction for financial institutions to do a good job in pension finance and provided fundamental guidelines for action.

1. Our country accelerates into the aging age

In 2020, the elderly population over 65 years old accounted for 15%, according to the current population development trend, it is expected that by 2050, the elderly population over 65 years old will account for 30%, and with the development of medical technology, the average life expectancy will reach 78 years in 2021, and it is expected that the average life expectancy will reach 84 years in 2050.

Figure 1: The aging trend of the population is obvious, and the age of longevity is coming

With the continuation of fewer children and low fertility rate, the pressure of social pension will be further intensified. In 2022, the natural population growth rate will be negative 6 per thousand, which is the second negative population growth since the Great Famine era in 1962. In 2020, the old-age dependency ratio is basically five young people raising one elderly person, and it is expected that by 2050, it will be two young people raising one elderly person. The trend of fewer people paying into pensions now and more people paying into pensions in the future is very striking.

Figure 2: Fewer children and low birth rate further aggravate the pressure of social pension

Compared with the international level, China’s total pension reserves are very insufficient, our current ratio and the country’s total GDP ratio is only 3%, while the ILO average level of 14%, we are still less than a quarter. At the same time, the international warning line for the pension replacement rate is 55%, and China has dropped to 37% in 2021. It can be seen that the current pension replacement rate is also very worrying.

Figure 3: Compared with the international average, China’s total pension reserves are insufficient and the pension replacement rate is low

In 2022, the third pillar of the pension system will be implemented, which is a good start, but compared with the United States, the third pillar of the United States accounts for 34.6%, nearly one-third, and we only have four out of 100,000, which is a very inadequate level. In addition, we have a pilot of personal pension, at present, only 8% of the population has full coverage of the three pillars, and only 83% of the basic pension, which shows that people do not pay attention to the need for individuals to save for pension. CXO UNION-CXO联盟(cxounion.cn)

Figure 4: Prepare for a rainy day, improve the construction of the pension system and accelerate the development of the third pillar

2. China Merchants Bank’s pension finance practice

China Merchants Bank regards pension finance as one of the eight characteristic finance of China Merchants Bank. In addition, combined with the three stages of individual pension, China Merchants Bank provides different tools and services. In the old age preparation stage, relatively young people prepare for their old life in advance, there are personal pension business, pension products on the shelves. If the customer has reached the retirement age and belongs to the old age stage, we need to work with various organizations to provide customers with services in the elderly community and elderly life. For some wealth inheritance of the elderly, there are family trust and pension trust tools and products.

From the perspective of the third pillar personal pension account opening, there are now 50.94 million people in the whole market who have opened accounts, and the current number of accounts opened by China Merchants Bank is 4.738 million. From the deposit amount, the whole market deposited 26.8 billion yuan, the average household deposited 2000 yuan, the amount deposited through the bank is 6.37 billion yuan, the average household deposited 7268 yuan. CXO UNION-CXO联盟(cxounion.cn)

Take a look at the customer’s choice of pension products.

The total amount of pension financing is only 100.4 billion, accounting for only about 40% of the total market, which indicates that pension products account for a very low proportion in the products of various asset management institutions, and it is also very insufficient. Although this is a very big market, we need to work together in the future; Pension finance accounts for only about 3/1000 of the total market financial products. Insurance, pure commercial pension insurance is even less, accounting for only about 3 ‰ of the total market.

Our conclusions are as follows:

First, open more accounts and pay less, highlighting that the awareness of pension needs to be improved. From October 2022 to the present, personal pensions have shown an inverted pyramid structure of “opening an account – paying a contribution – investing”, with more than 40 million account holders and only more than 10 million deposits, with the amount of each household contributing only more than 2,000 yuan. It can be seen that everyone’s investment awareness in this area is relatively weak.

Second, the ceiling on personal pension accounts is low. Japan’s personal pension account (tax-free) limit is 816,000 yen (about 160,000 yuan); The US 401k annual contribution limit is $66,000 (about 470,000 yuan); China’s personal pension (tax-free) limit is only 12,000 yuan.

Third, there are fewer types of pensions, which are roughly three or three per thousand.

Fourth, the characteristics of pension products are not outstanding. Taking pension funds as an example, there are 179 pension funds at present, only 10 have achieved positive returns, and among the products with negative returns, the fund with the biggest loss has a return of -18.38%. This makes individual investors worried, and in turn, they reject pension products.

3. Jointly do a good job of pension finance “big article”

This “big article” of pension finance needs the joint efforts of the whole industry. Specifically:

In terms of policy support, more support policies need to be introduced, including financial subsidies and interest discounts for low-income people, tax relief for pension products, and raising the tax-free contribution ceiling for personal pensions. At the national level, we must increase publicity efforts, including improving residents’ awareness of risk prevention and strengthening residents’ awareness of old-age care. In terms of regulatory guidance, some effective guidance must be carried out from the regulatory level to encourage various financial institutions to vigorously invest in the field of pension finance. CXO UNION-CXO联盟(cxounion.cn)

For various fields and industries, the banking industry, we think that the focus is on specific pension target financial management, can use housing reverse mortgage and other ways to help you inject some sources of pension funds.

In the insurance industry, in addition to Taikang’s community pension, there are now many insurance companies in this field. We think there are still a lot of big articles to do in the future, including home care for the elderly, disabled and mentally retarded elderly care and nursing care for the elderly.

The fund industry, in addition to expanding and strengthening the direction of pension target funds, has relatively large space in pension industry guidance funds and equity funds.

From the perspective of the trust industry, the focus is on special purpose trusts, such as pension trusts, which also have great market potential.

In the last word, finance should also move forward hand in hand, forge ahead, and the whole industry should work together to write a “big article” on pension finance, and jointly meet the beautiful era of pension finance. CXO UNION-CXO联盟(cxounion.cn)

由CXO UNION-CXO联盟(cxounion.cn)转载而成,来源于中国财富管理50人论坛;编辑/翻译:CXO UNIONCXO联盟小U。

如需加入CXO UNION(CXO联盟)高管社群,请联系社群小伙伴哦~

免责声明: 本网站(http://www.cxounion.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。

如需加入CXO UNION(CXO联盟)高管社群,请联系社群小伙伴哦~

免责声明: 本网站(http://www.cxounion.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。

Search

Popular Posts

-

2024数字化灯塔案例评选申报开启!

“2024数字化灯塔案例评选”于3月正式启动,诚挚欢迎业界同仁自荐和推荐,一起推动产业数字化进程,助力赋能企业…

-

2024 X-Award星盘奖申报通道已开启!

X-Award星盘奖是数字化转型服务、IT服务行业重要的商业奖项,旨在表彰行业里提供杰出数字化转型服务与IT服…

-

2024 N-Award星云奖申报通道已开启!

N-Award是数字化转型领域重要的商业奖项,旨在表彰那些以非凡的远见、超群的领导才能和卓越的成就来激励他人的…